Estimating the Per-Person Economic Burden of Extreme Weather, Insurance Destabilization, Climate Inflation, and Health Impacts

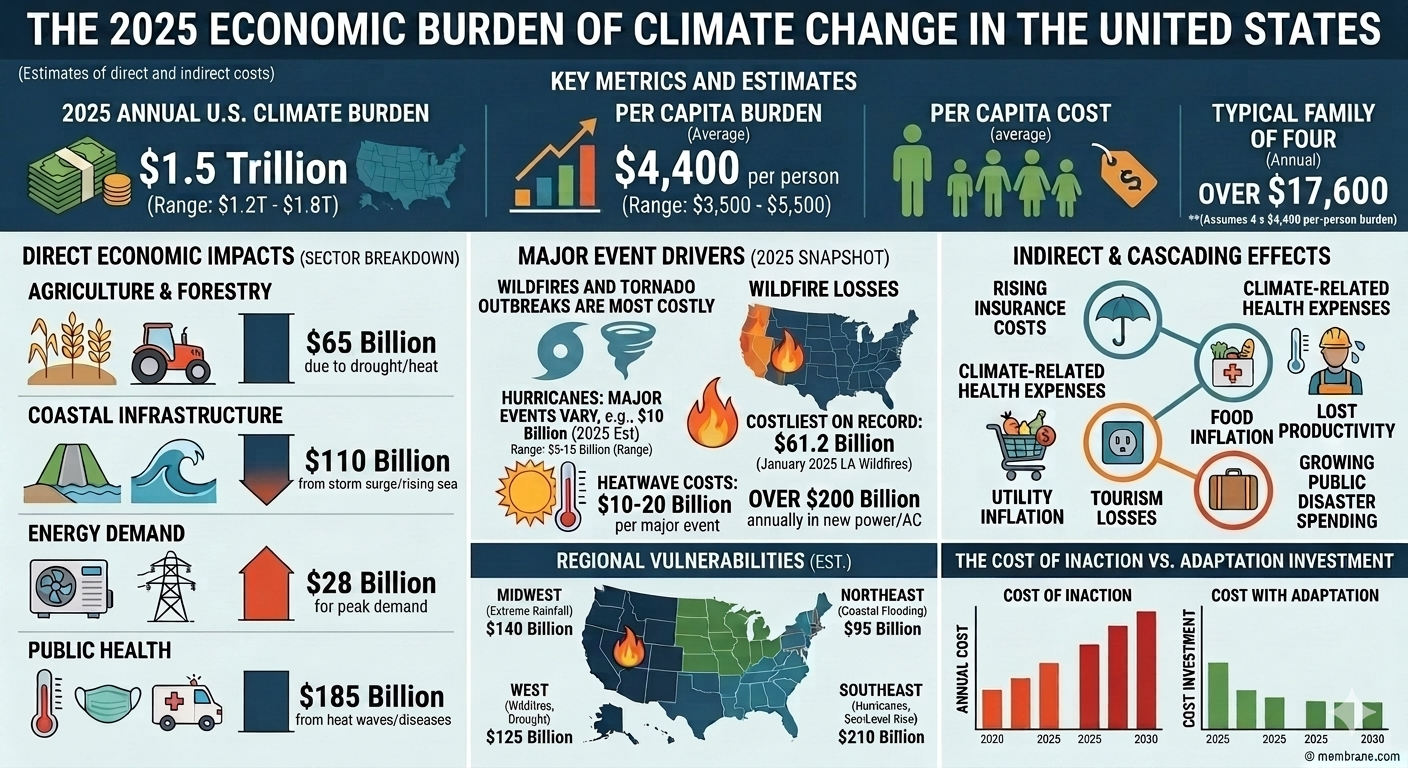

A reasonable all-in estimate for the 2025 economic burden of climate change on the United States is about $1.5 trillion, or roughly $4,400 per person. For a family of four, the implied annual burden is roughly $17,600. That burden extends far beyond direct disaster losses and includes rising insurance costs, climate-related health expenses, food and utility inflation, lost productivity, tourism losses, and growing public disaster spending.

By Daniel Brouse and Sidd Mukherjee

Abstract

Climate change in the United States is no longer best understood solely as an environmental problem or a tally of disaster losses. It has become a broad economic burden imposed on households, businesses, insurers, healthcare systems, and governments through multiple overlapping channels. In 2025, this burden extended far beyond direct storm, wildfire, flood, and heat damage. It also appeared in rising property-insurance costs, housing-market instability, climate-driven health expenses, higher utility bills, food inflation, tourism losses, public disaster spending, and reduced labor productivity.

This paper presents a bottom-up estimate of the all-in 2025 economic cost of climate change in the United States, with the goal of approximating the average cost per person when both direct and indirect burdens are considered. Because no official ledger exists for “total climate costs,” the analysis aggregates seven major categories of climate-related economic burden: (1) direct disaster damages, (2) property insurance and real-estate destabilization, (3) healthcare and health-insurance costs, (4) climate-driven inflation in food, utilities, and supply chains, (5) tourism and recreation losses, (6) government expenditures and public borrowing strain, and (7) productivity losses and business interruption.

Using a U.S. population of approximately 340 million, the paper estimates a 2025 climate burden of roughly $1.5 trillion, with a plausible range of $1.2 trillion to $1.8 trillion. On a per-person basis, this implies an average cost of approximately $4,400 per American in 2025, with a conservative range of $3,500 to $5,500 per person. For a family of four, the implied annual burden is roughly $17,600.

The core conclusion is that climate change now functions as a diffuse but powerful economic tax on American life. It raises insurance premiums, erodes home values, inflates electricity and food costs, worsens public-health burdens, strains local and federal budgets, and lowers productivity. Even when households are not directly hit by a flood, wildfire, or hurricane, they increasingly pay for climate change through the price system, the insurance system, the healthcare system, and the tax system. Climate change in the United States is therefore not just a future risk; it is already a major annual cost center embedded in the daily economy.

1. Introduction

Public discussion of climate change in the United States often focuses on dramatic physical events: hurricanes, floods, wildfires, heatwaves, droughts, and billion-dollar disasters. While those events are important, they capture only part of the actual economic burden climate change now imposes. The larger story is that climate disruption has begun to function as a system-wide cost escalator. It increases insurance premiums, weakens housing markets, strains public infrastructure, raises electricity demand, amplifies health expenses, disrupts supply chains, and inflates food prices. In short, climate change is no longer merely a source of episodic disaster losses. It is increasingly a permanent drag on household finances and national economic stability.

This distinction matters because the official accounting of climate damages remains incomplete. Annual disaster-loss tallies typically capture only direct physical damage: insured losses, destroyed structures, infrastructure repair, and some immediate business interruption. They generally do not capture the full downstream cost of heat-related illness, wildfire smoke exposure, insurance market retreat, declining property values in flood-prone communities, higher grocery bills caused by weather-related crop disruption, or the fiscal burden of repeated emergency appropriations. The result is that climate change is often underestimated as an economic force because the damage is fragmented across categories that are normally tracked separately.

The goal of this paper is to estimate the average cost per person in the United States due to climate change in 2025, including both direct and indirect costs. Rather than looking only at disaster damages, the paper uses a broader economic framework that includes the channels through which climate risk is already transmitted into everyday life. These channels include property insurance and housing destabilization, healthcare costs, health-insurance pressure, climate-driven inflation, lost tourism revenue, public fiscal strain, and lost productivity.

The premise is simple: if climate change is now affecting the economy through multiple systems at once, then measuring its burden requires more than adding up burned homes and flooded roads. It requires asking how much climate disruption is already embedded in the bills Americans pay, the risks they insure, the taxes they fund, the wages they lose, and the wealth they fail to preserve.

This paper estimates that the total 2025 climate burden on the United States was approximately $1.5 trillion, or roughly $4,400 per person. That estimate is necessarily approximate, because some categories—especially climate-related inflation and property-value impairment—cannot be measured with perfect precision. But even under conservative assumptions, the results point in the same direction: climate change is already costing the average American several thousand dollars per year, whether or not they realize it.

2. Methodology: A Bottom-Up Estimate of the 2025 Climate Burden

There is no single official database that reports the “total cost of climate change” for a given year in the United States. Any attempt to estimate that figure must therefore combine multiple categories of loss and cost transmission. The central methodological challenge is to build a broad estimate without double-counting the same damage in multiple places.

To address that, this paper separates climate costs into seven major categories and treats each as an incremental climate-attributable burden rather than as a total category expenditure. The categories are:

- Direct disaster damages

- Property insurance and real-estate destabilization

- Healthcare and health-insurance costs

- Climate-driven inflation in food, utilities, and supply chains

- Tourism and recreation losses

- Government expenditures and fiscal strain

- Productivity losses and business interruption

The logic is not that all food inflation, all insurance inflation, or all healthcare spending is caused by climate change. Rather, the question is: what share of these burdens in 2025 can plausibly be attributed to climate disruption? The estimate therefore focuses on the incremental climate component of each category.

Using a U.S. population of 340 million, the paper translates each category’s national cost into a per-person burden. The final total is presented as a range, with a central estimate used for the headline figure.

3. Direct Disaster Damages: The Visible but Incomplete Baseline

The most visible component of climate cost is direct disaster damage: destroyed homes, burned neighborhoods, damaged roads, downed power lines, emergency response costs, and insured losses from floods, storms, wildfires, and other extreme events. These costs are widely reported because they are dramatic, immediate, and often insurable.

For 2025, a reasonable national baseline for direct disaster damages is approximately $115 billion. This reflects the year’s major climate-related disasters, including catastrophic wildfires, severe storms, flooding, and other billion-dollar events. That total is useful because it anchors the analysis in a concrete measure of visible physical damage.

But direct disaster losses are only the beginning of the story. They do not include most health impacts from wildfire smoke and extreme heat, much of the uninsured or underinsured damage absorbed by households, long-term property-value erosion in high-risk areas, or the broad inflationary effects of weather disruption on food and energy. Disaster losses therefore function here as a baseline floor, not a complete accounting of climate cost.

Using a population of 340 million, $115 billion in direct losses translates to roughly:

($115 billion) / (340 million) ≈ $338 per person

That figure is significant, but it is also misleadingly small if treated as the total climate burden. The rest of the paper shows why.

4. Property Insurance and Real-Estate Destabilization

4.1 Insurance premiums as climate transmission mechanisms

One of the clearest ways climate change now enters household budgets is through the property insurance market. As wildfire risk, hurricane losses, inland flooding, and severe convective storms intensify, insurers have raised premiums sharply, tightened underwriting standards, reduced coverage, or exited some markets entirely. These changes are not merely administrative adjustments. They are a direct financial transmission of climate risk into household cash flow.

By 2025, homeowners across the United States were already facing significantly higher insurance costs than they paid only a few years earlier. National average homeowners insurance premiums had risen sharply since 2021, outpacing wage growth and standard inflation. In high-risk states, the increases were much more severe. This means climate change is no longer just a future threat to homeownership. It is already a monthly budget issue.

To estimate the climate-driven premium burden, this paper assumes that a substantial portion of recent premium growth reflects climate-related risk repricing. With approximately 86 million owner-occupied households in the United States, even a few hundred dollars of annual climate-attributable premium increase per household produces tens of billions of dollars in national burden.

A rough estimate of the incremental 2025 climate-driven homeowners insurance burden is approximately $47 billion.

4.2 The “protection gap” and uninsured losses

Premium increases are only part of the cost. The larger and more dangerous issue is the protection gap: the widening difference between total physical losses and the portion actually covered by insurance. As climate disasters intensify, insurers increasingly protect themselves by raising deductibles, limiting coverage, or leaving risky markets altogether. The losses do not disappear. They are simply transferred to homeowners, renters, local governments, state residual insurance pools, and federal taxpayers.

This means a major disaster can impose large economic costs even when insurance coverage appears to exist on paper. Deductibles, exclusions, underinsurance, and uninsured property losses all create direct household financial stress. Local governments may also absorb part of the burden through emergency repairs, temporary housing, and infrastructure response.

For 2025, this paper estimates the protection gap and related uninsured burden at roughly $100 billion to $180 billion.

4.3 Property value impairment and housing-market destabilization

Climate change also erodes housing wealth through a slower mechanism: property repricing. Homes exposed to repeated flooding, wildfire smoke, chronic coastal inundation, or rapidly rising insurance costs become harder to insure, harder to finance, and harder to sell. Even if a home is not destroyed, the expected future cost of owning it can rise enough to depress its market value.

This effect matters because American household wealth is deeply tied to home equity. When climate risk begins to reduce resale value or increase carrying costs, the result is not merely a “real-estate issue.” It becomes a balance-sheet problem for households and a tax-base problem for municipalities.

Because these losses are diffuse and difficult to observe in real time, they are often excluded from climate accounting. Yet they are economically real. This paper conservatively assigns $100 billion to $170 billion in 2025 property-value impairment and housing-market friction costs attributable to climate exposure.

4.4 Total property and housing burden

Combining premium increases, protection-gap losses, and property-market destabilization, the total 2025 property insurance and real-estate climate burden is estimated at:

$250 billion to $400 billion

On a per-person basis, that implies:

($250 billion) / (340 million) ≈ $735 per person

to

($400 billion) / (340 million) ≈ $1,176 per person

This is one of the largest and most direct climate burdens already visible in the household economy.

5. Healthcare and Health Insurance Costs

Extreme weather does not stop at property damage. It also leaves a major financial footprint in the healthcare system. Climate-related health burdens include emergency-room visits during heatwaves, hospitalizations from smoke exposure, respiratory and cardiovascular stress during wildfire events, injuries during storms and floods, mental-health impacts from displacement and repeated disaster exposure, and rising claims associated with climate-sensitive disease patterns.

Extreme heat is especially important because it is already one of the deadliest weather-related hazards in the United States. It contributes to dehydration, kidney stress, cardiovascular strain, respiratory distress, pregnancy complications, and dangerous workplace conditions. Wildfire smoke adds another layer of harm by exposing millions of people to fine particulates and toxic compounds that can worsen asthma, heart disease, and lung injury.

These health burdens create costs through several channels:

- direct medical treatment,

- increased emergency-room utilization,

- public-health response,

- higher health-insurance claims,

- employer healthcare costs,

- lost workdays and reduced labor capacity.

The financial burden of these impacts is not fully visible in standard disaster-loss reporting because many of the costs are absorbed later through hospitals, insurers, employers, Medicare, Medicaid, and household medical bills. In effect, climate change raises healthcare costs not only by causing acute disasters, but by amplifying the baseline disease and treatment burden associated with heat and air pollution.

This paper estimates the incremental 2025 climate-related health and health-insurance burden at approximately:

$100 billion to $180 billion

Per person, that implies roughly:

$294 to $529 per person

A central estimate of $140 billion is reasonable for 2025, particularly given the scale of smoke exposure, heat stress, and extreme-weather-related healthcare disruptions.

6. Climateflation: Food, Utilities, and Supply-Chain Costs

6.1 Climate change as a hidden tax on household consumption

One of the most important and least appreciated channels of climate cost is inflation. Climate change increasingly acts as a hidden tax on everyday life by raising the cost of food, electricity, logistics, and consumer goods. This is not because climate change explains all inflation. It does not. But it does increase price pressure through several pathways:

- drought and flood damage to crops,

- livestock heat stress,

- water shortages,

- higher cooling demand,

- power-grid strain,

- storm-related transport disruption,

- warehouse and refrigeration costs,

- spoilage and inventory loss,

- interruptions to rail, trucking, and river transport.

These pressures feed into the price system even for households that never experience a direct disaster. Climate change therefore affects family budgets not just through insurance or emergency repairs, but through recurring monthly bills for groceries, utilities, and goods whose supply chains are increasingly exposed to weather disruption.

6.2 Utility cost increases from heat

Persistent summer heatwaves raise electricity demand as homes, offices, warehouses, and hospitals rely more heavily on air conditioning. Utilities must manage higher peak demand, more stressed transmission systems, and sometimes reduced efficiency of generation and delivery infrastructure during extreme heat. These costs are passed on through higher rates, fuel adjustments, and capacity charges.

A reasonable estimate for the 2025 climate-attributable utility burden is $60 billion to $100 billion.

6.3 Food inflation and agricultural volatility

Food prices are especially vulnerable to climate disruption. Droughts, floods, heatwaves, and shifting seasonal conditions affect crop yields, planting schedules, water availability, livestock productivity, storage costs, and transport reliability. When these disruptions occur across multiple regions or commodity groups, the effect compounds. The result is not just one bad harvest, but persistent volatility across the food system.

This paper conservatively estimates that $250 billion to $350 billion of the 2025 consumer food-price burden can be attributed to climate-related agricultural and supply-chain disruption.

6.4 Supply-chain and logistics pass-through

Climate disruption also raises costs through business interruption, transportation delays, warehouse cooling expenses, spoilage, shipping rerouting, and inventory risk. These are eventually passed on to consumers and businesses across the economy.

For 2025, this paper assigns $180 billion to $250 billion to the broader supply-chain and logistics burden associated with climate disruption.

6.5 Total climateflation burden

Combining utilities, food inflation, and logistics pass-through, the total 2025 climateflation burden is estimated at:

$500 billion to $700 billion

Per person, that equals roughly:

$1,470 to $2,059 per person

This makes climateflation the single largest category in the 2025 climate burden estimate.

7. Tourism and Recreation Losses

Climate change also imposes substantial costs on local and regional economies that depend on tourism and outdoor recreation. Extreme heat, wildfire smoke, coastal flooding, beach erosion, poor snow conditions, storm damage, and unpredictable seasonal patterns all reduce tourism demand and disrupt recreation-dependent businesses.

Examples include:

- park closures due to wildfire or heat,

- canceled outdoor festivals and events,

- lower visitation to smoke-affected regions,

- shortened or erratic ski seasons,

- damage to coastal tourism infrastructure,

- lost restaurant, hotel, and service-sector revenue in climate-affected destinations.

These losses may seem secondary compared with insurance or health costs, but in many regions they are economically important. A canceled tourism season can mean lost wages, reduced sales-tax revenue, weakened hotel occupancy, and stress on small businesses already operating with narrow margins.

For 2025, this paper estimates the climate-related tourism and recreation burden at:

$20 billion to $40 billion

Per person, that is approximately:

$59 to $118 per person

8. Government Expenditures and Fiscal Strain

Taxpayers also bear a major share of the climate burden through public spending and public finance. Disaster relief, emergency housing, infrastructure repair, wildfire suppression, flood control, insurance backstops, and local recovery grants all require funding. These costs may be spread across federal, state, and local budgets, but they are ultimately part of the economic burden climate change imposes on the public.

In addition to direct spending, climate risk can increase the cost of borrowing for local governments. Municipal bond investors and credit-rating agencies increasingly evaluate physical climate vulnerability when assessing long-term fiscal risk. Communities facing repeated flooding, wildfire exposure, or insurance-market stress may face higher borrowing costs for roads, water systems, schools, and other routine infrastructure.

The public climate burden therefore has two components:

- direct fiscal spending on response, repair, and recovery, and

- higher structural financing costs for climate-exposed jurisdictions.

This paper estimates the 2025 public-sector climate burden at:

$80 billion to $120 billion

Per person, that equals roughly:

$235 to $353 per person

9. Productivity Losses and Business Interruption

A final major category is the cost of lost work, reduced productivity, and interrupted business activity. Extreme heat reduces labor output, especially in construction, agriculture, warehousing, delivery, transportation, and other outdoor or non-climate-controlled sectors. Wildfires and smoke events can shut down worksites and keep customers home. Floods and storms interrupt logistics, force evacuations, close schools, and disrupt childcare arrangements that allow people to work.

These losses matter because they spread climate costs through the labor market even when no major asset is destroyed. A family may lose income because a parent misses work during a flood recovery or because a heatwave reduces available hours. A small business may lose revenue because smoke or road closures keep customers away. A local economy may lose millions in output because transport links or utility systems fail during extreme weather.

This paper estimates the 2025 productivity and business-interruption burden at:

$120 billion to $220 billion

Per person, that equals approximately:

$353 to $647 per person

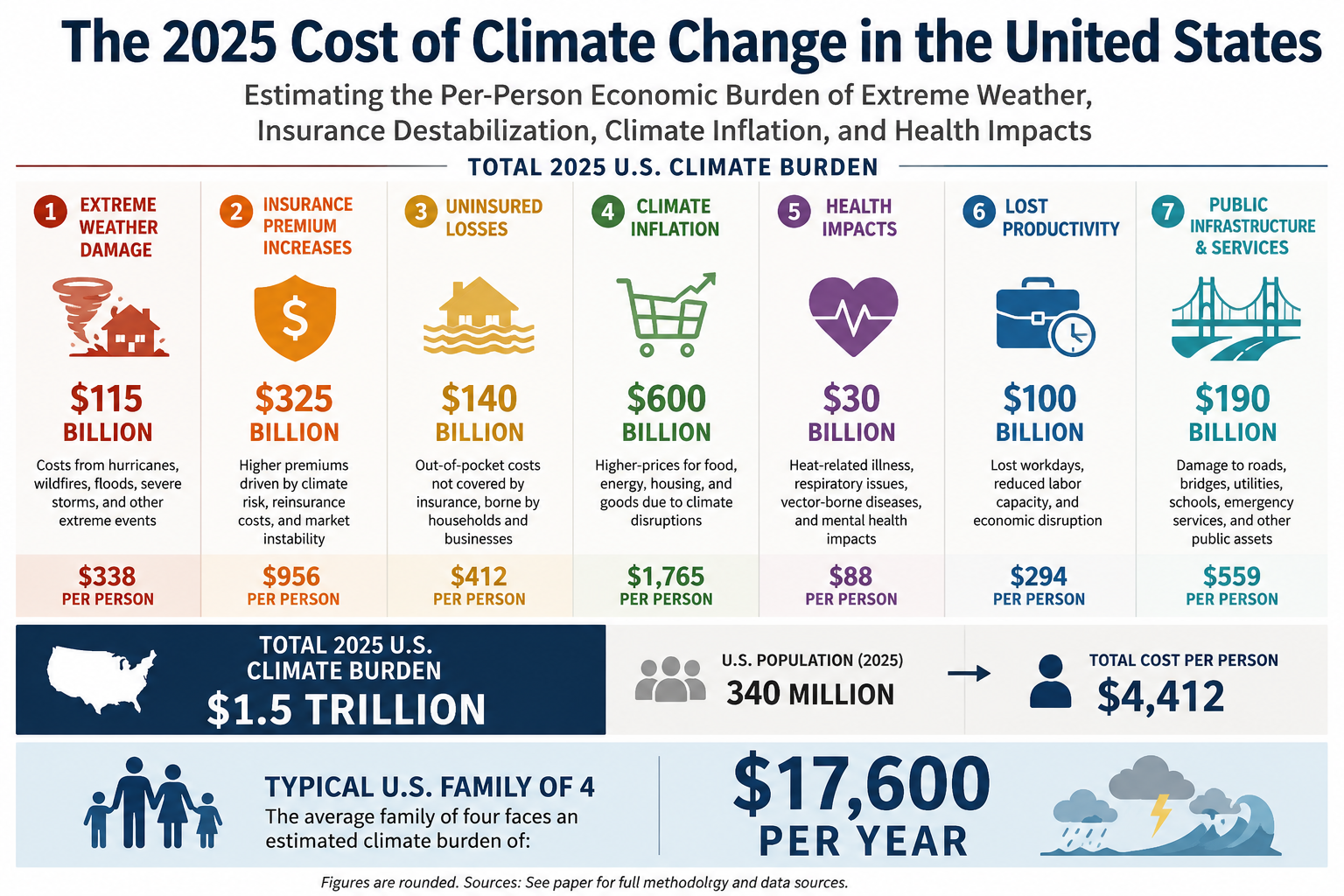

10. Summary Table: The 2025 Climate Burden in the United States

| Category | Estimated 2025 U.S. climate cost | Per person |

|---|---|---|

| Direct disaster damages | $115 billion | $338 |

| Property insurance + real-estate destabilization | $250–$400 billion | $735–$1,176 |

| Healthcare + health insurance | $100–$180 billion | $294–$529 |

| Climateflation (food, utilities, supply chains) | $500–$700 billion | $1,470–$2,059 |

| Tourism + recreation losses | $20–$40 billion | $59–$118 |

| Government expenditures + fiscal strain | $80–$120 billion | $235–$353 |

| Productivity losses + business interruption | $120–$220 billion | $353–$647 |

11. Central Estimate

Using the midpoint of each category yields the following 2025 estimate:

| Category | Midpoint |

|---|---|

| Direct disaster damages | $115 billion |

| Property insurance / housing destabilization | $325 billion |

| Healthcare / health insurance | $140 billion |

| Climateflation | $600 billion |

| Tourism / recreation | $30 billion |

| Government / fiscal strain | $100 billion |

| Productivity / business interruption | $190 billion |

Total:

115 + 325 + 140 + 600 + 30 + 100 + 190 = 1,500 billion

This implies a total 2025 U.S. climate burden of approximately $1.5 trillion.

Dividing by a U.S. population of 340 million:

$1.5 trillion ÷ 340 million ≈ $4,412 per person

Rounded to the nearest hundred dollars:

Average 2025 climate cost per person in the United States: approximately $4,400

A reasonable conservative range is $3,500 to $5,500 per person.

For a family of four, that implies a total annual burden of approximately:

4 × $4,400 = $17,600

12. Discussion: Climate Change as an Economic Tax on American Life

The most important implication of this analysis is that climate change is already functioning as a diffuse economic tax on American life. It is not merely a matter of future risk or isolated disaster recovery. It now affects the economy through the insurance system, the housing system, the healthcare system, the utility system, the food system, and the tax system.

Most Americans will not experience the climate burden as a single line item. They will experience it as a set of pressures that appear unrelated at first glance:

- a higher homeowners insurance premium,

- a larger health-insurance renewal,

- an unusually high summer electric bill,

- more expensive groceries,

- rising local taxes for infrastructure repair,

- difficulty selling a flood-prone property,

- missed work after a smoke event or flood,

- a vacation canceled by heat, fire, or storm damage.

Taken separately, these costs may seem manageable or even invisible. Taken together, they form a substantial and growing transfer of wealth away from households and toward damage control, adaptation, emergency response, and loss absorption.

The burden also falls unevenly. Households in coastal areas, wildfire corridors, heat-prone cities, drought-exposed agricultural regions, and flood-prone inland communities often bear a much larger share than the national average. Lower-income households are especially vulnerable because they have less capacity to absorb rising insurance costs, medical bills, evacuation expenses, or repeated utility shocks. In that sense, climate change is not only an environmental stressor and an economic stressor. It is also a force that can widen inequality by imposing the heaviest burden on those with the thinnest financial buffers.

13. Conclusion

This paper estimates that the 2025 cost of climate change in the United States was approximately $1.5 trillion, equal to roughly $4,400 per person or $17,600 for a family of four. A conservative range of $3,500 to $5,500 per person captures the uncertainty in the estimate while still underscoring the scale of the burden.

The key point is not the false precision of any single number. It is the recognition that climate change now imposes a broad, recurring, and deeply embedded economic burden on the United States. Direct disaster damages remain important, but they are only one part of the story. The larger burden increasingly arrives through rising insurance costs, real-estate destabilization, health expenses, climate-driven inflation, tourism losses, public fiscal strain, and lost productivity.

In other words, climate change is no longer simply something Americans pay for after a disaster. It is something they are already paying for every month—through their premiums, utility bills, grocery receipts, taxes, healthcare costs, and weakened property values. The economic question is no longer whether climate change is expensive. It is how much of the American cost of living is now being quietly shaped by it.

Sources List

1. U.S. Billion-Dollar Disaster Data (Core Economic Loss Foundation)

- Smith, A. (2026). U.S. Billion-Dollar Weather and Climate Disasters in 2025. Climate Central.

https://www.climatecentral.org/climate-services/billion-dollar-disasters - National Centers for Environmental Information (NCEI), NOAA. (2025). Calculating the Cost of Weather and Climate Disasters.

https://www.ncei.noaa.gov/news/calculating-cost-weather-and-climate-disasters - Smith, A. (2025). 1980–2024 U.S. Billion-Dollar Weather and Climate Disasters (Technical Report). NOAA/NCEI.

https://www.ncei.noaa.gov/access/billions/

2. Aggregate National Economic Loss Trends

- Climate Central. (2025). U.S. Billion-Dollar Disasters: 1980–2024.

https://www.climatecentral.org/climate-matters/billion-dollar-disasters-2025 - Climate Central. (2025). 2025 in Review: U.S. Billion-Dollar Disasters.

https://www.climatecentral.org/climate-matters/2025-in-review

3. Insurance Market Impacts & Insured Losses

- Swiss Re Institute. (2025). Global natural catastrophe insured losses outlook (2025). Reuters summary.

https://www.reuters.com/sustainability/climate-energy/costs-climate-disasters-reach-145-bln-2025-says-swiss-re-2025-04-29/ - Aon. (2025). Global Catastrophe Losses Report (2025). Financial Times summary.

https://www.ft.com/content/bc5fa1ea-c11f-47bb-a085-ec85cc6a4448

4. Economic Damage Attribution & Climate Change Drivers

- U.S. Environmental Protection Agency (EPA), National Center for Environmental Economics. (2025). Economic Damages from Climate Change to U.S. Populations.

https://www.rff.org/publications/external-resources/national-center-for-environmental-economics-economic-damages-from-climate-change-to-us-populations/ - Climate Central. (2025). U.S. Billion-Dollar Weather and Climate Disasters (Methodology & Drivers).

https://www.climatecentral.org/climate-services/billion-dollar-disasters/time-series

5. Macroeconomic & Integrated Climate Damage Literature

- Kopits, E. et al. (2025). Economic Impacts of Climate Change in the United States: Integrating and Harmonizing Evidence from Recent Studies.

https://arxiv.org/abs/2509.00212 - Tol, R. S. J. (2022). A Meta-analysis of the Total Economic Impact of Climate Change.

https://arxiv.org/abs/2207.12199

6. Climate Adaptation and Insurance System Stress

- Josephson, A. et al. (2024). The Economics of Climate Adaptation: An Assessment.

https://arxiv.org/abs/2411.16893

7. Supporting Media & Risk Communication (Contextual Evidence)

- Live Science. (2025). Extreme weather caused more than $100 billion in damage in first half of 2025.

https://www.livescience.com/planet-earth/climate-change/extreme-weather-caused-more-than-usd100-billion-in-damage-by-june-smashing-us-records