Macro-Welfare Frameworks vs. Economic Justice Valuation in the United States

Daniel Brouse and Sidd Mukherjee

I. Introduction

A. Research Problem

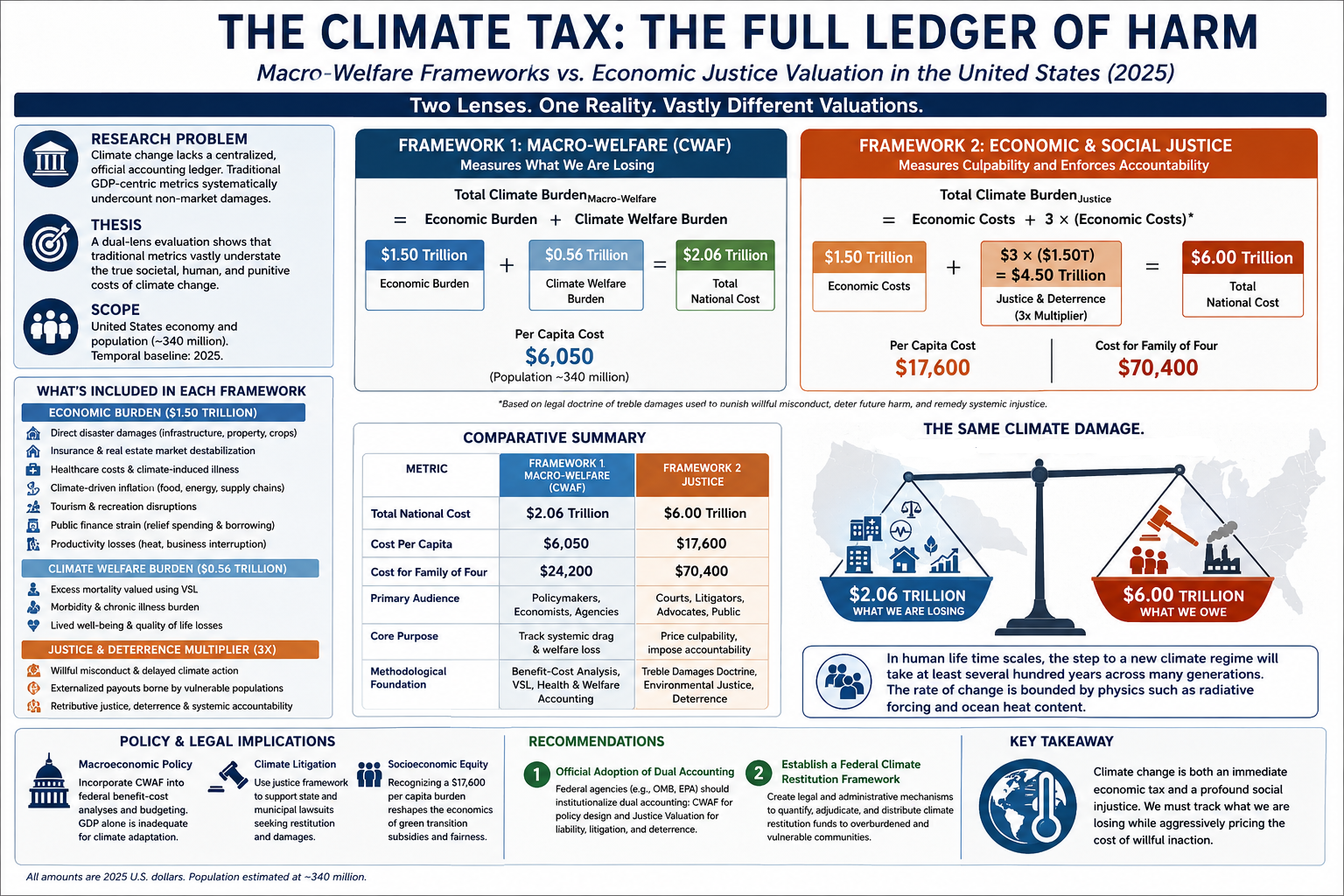

Climate change imposes large and growing costs on the United States, yet there is still no centralized national ledger that captures the full burden in a unified way. Conventional economic indicators—especially GDP, insured losses, and direct disaster tallies—systematically undercount the real cost of climate disruption because they omit or minimize non-market harms such as premature mortality, reduced life expectancy, chronic illness, degraded quality of life, ecological destabilization, and the unequal distribution of climate damages across vulnerable populations.

A narrow GDP-centered framework also fails to capture a second dimension of climate cost: accountability. A large share of today’s climate burden is not simply the product of random weather volatility. It is the cumulative result of delayed mitigation, externalized damages, underpriced emissions, regulatory failure, and in some cases decades of deception regarding the risks of fossil-fuel dependence. That means climate accounting must confront not only what climate change is costing the economy, but also what it should cost under a framework of social justice and deterrence.

B. Thesis Statement

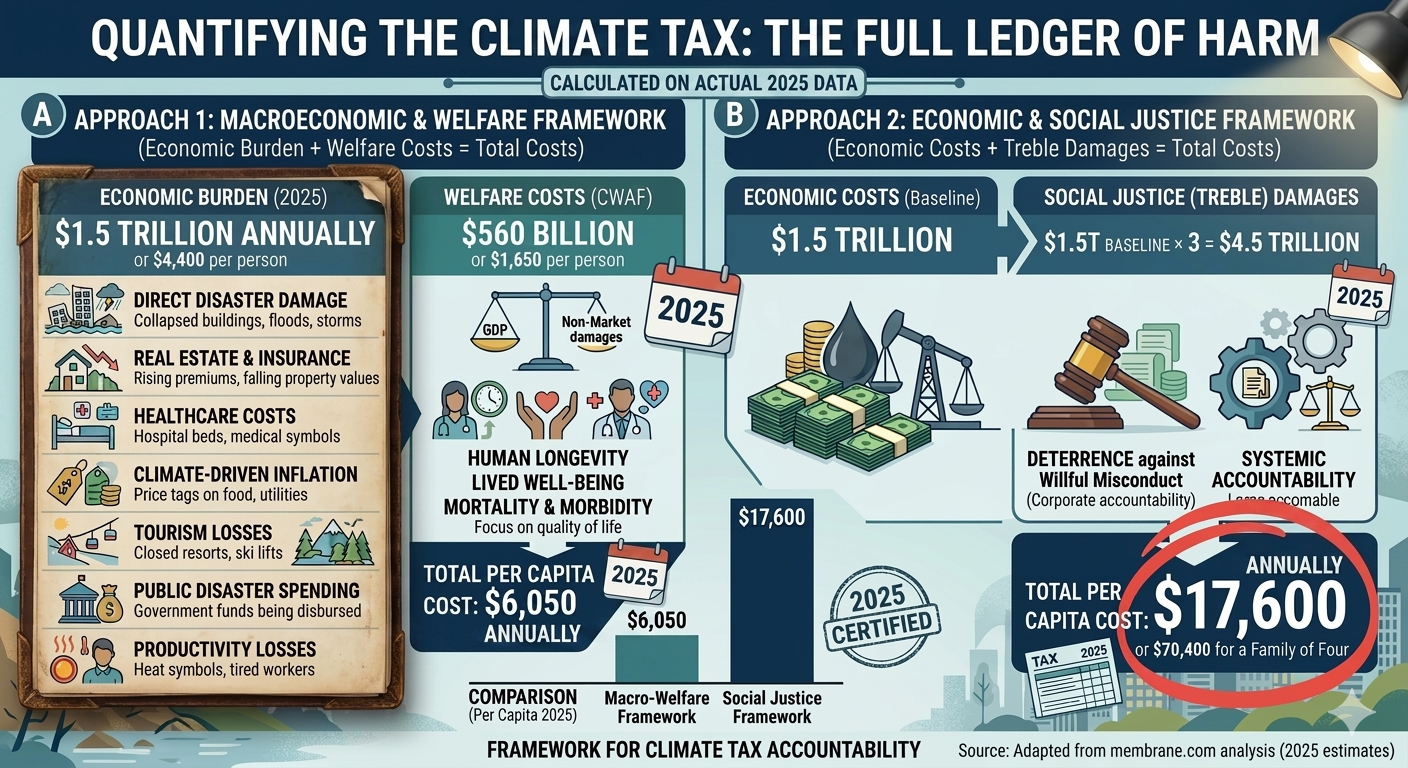

Evaluating the 2025 U.S. cost of climate change requires moving beyond direct disaster losses and beyond GDP-centered accounting. Using a dual-lens approach, it compares:

- a Macroeconomic and Welfare Framework, which estimates the 2025 U.S. climate burden at approximately $2.06 trillion, or about $6,050 per person, and

- an Economic and Social Justice Framework, which applies a treble-damages logic to climate-linked economic harms and yields a 2025 burden of approximately $6.0 trillion, or about $17,600 per person.

The core claim is that traditional economic metrics substantially understate the true societal burden of climate change. Climate damages should be understood not only as macroeconomic drag and welfare erosion, but also as a form of externalized injury with distributive, ethical, and potentially punitive dimensions.

C. Scope of the Study

This study focuses on the United States in calendar year 2025. Per-capita values are based on a U.S. population baseline of approximately 340 million residents. The analysis is national rather than state-specific and is intended as a high-level accounting framework rather than a final litigation damages model.

II. Methodology 1: The Macroeconomic and Welfare Framework

A. Conceptual Architecture

The first framework combines two components:

- Economic burden: the direct and indirect market-facing costs imposed by climate change in 2025; and

- Climate welfare burden: the non-market human costs associated with mortality, life-expectancy loss, morbidity, and degraded quality of life.

The core accounting identity is:

Total Climate Burden (Macro-Welfare) = Economic Burden + Climate Welfare Burden

For 2025, the study uses the following central values:

$1.50T + $0.56T = $2.06T

On a per-capita basis:

$2.06T / 340M = $6,059 ≈ $6,050 per person

This can also be expressed as:

$4,400 + $1,650 = $6,050

where:

- $4,400 per person is the estimated economic burden, and

- $1,650 per person is the estimated climate welfare burden.

B. The Economic Burden Baseline: $1.5 Trillion ($4,400 per Capita)

The economic burden baseline is designed to capture the direct and indirect market-facing cost of climate change in the United States in 2025. It includes seven broad categories of loss.

1. Direct disaster damages

This category includes physical destruction from hurricanes, inland flooding, wildfires, convective storms, drought-related losses, heat-related infrastructure damage, and other extreme-weather events. It covers residential, commercial, public-sector, insured, and uninsured losses.

2. Real estate and insurance destabilization

Climate change is increasingly priced into property markets and insurance markets through higher premiums, policy nonrenewals, shrinking insurability, reserve stress, and geographic repricing of risk. These effects act as a quasi-tax on households, businesses, and municipalities even in years without a single catastrophic event.

3. Healthcare and health-insurance costs

Heat stress, wildfire smoke, respiratory disease, cardiovascular strain, injuries, mental-health burdens, and other climate-related medical effects increase both direct healthcare spending and insurance costs. These costs are counted here only insofar as they represent market expenditures rather than welfare losses already captured separately in the climate welfare framework.

4. Climate-driven inflation and household cost pressure

Climate shocks increase the price of food, electricity, water, transportation, and household essentials through crop disruption, supply-chain interruption, infrastructure stress, and energy-demand spikes. These effects function as a hidden climate tax on households and are treated as part of the economic burden.

5. Tourism and recreation losses

Climate volatility disrupts beach economies, ski industries, lake and river recreation, outdoor events, park visitation, and seasonal tourism revenue. The direct revenue loss belongs in the economic burden, while the lost enjoyment and diminished lived experience belong more naturally in the welfare framework.

6. Public finance and fiscal burden

Federal, state, and local governments increasingly absorb climate costs through disaster relief, infrastructure repair, emergency response, insurance backstops, and climate-related borrowing. These expenditures represent real public resource costs even when financed through debt.

7. Productivity losses

Heat stress, smoke exposure, flooding, power outages, transportation interruption, and business downtime reduce labor productivity and economic output. These losses are among the most undercounted but economically significant climate costs.

Taken together, these categories produce a 2025 U.S. economic burden estimate of approximately $1.5 trillion.

On a per-capita basis:

$1.50T / 340M = $4,412 ≈ $4,400 per person

This figure is intended as an integrated estimate of the market-facing annual climate burden imposed on the United States in 2025.

C. The Climate Welfare Accounting Framework (CWAF): $560 Billion ($1,650 per Capita)

The second component of Framework 1 is the Climate Welfare Accounting Framework (CWAF), which measures the direct erosion of human well-being from climate change. CWAF is designed to capture losses that do not appear clearly in GDP or conventional market accounts, including premature mortality, reduced life expectancy, chronic morbidity, and diminished quality of life.

1. CWAF structure

CWAF is organized around three pillars:

- Pillar A: Mortality valuation

- Pillar B: Life-expectancy loss

- Pillar C: Morbidity and quality-of-life loss

The raw component identity is:

CWAF(raw) = A + B + C

Using the central estimates in this framework:

- A = $375B

- B = $80B

- C = $180B

So the raw component sum is:

$375B + $80B + $180B = $635B

However, because mortality, life-year loss, and morbidity estimates can overlap at the margins even after careful structuring, the framework applies a conservative overlap adjustment and presents a central CWAF estimate of approximately $560 billion rather than the full raw sum of $635 billion.

Thus:

- CWAF raw central estimate = $635B

- CWAF adjusted central estimate ≈ $560B

On a per-capita basis:

$560B / 340M = $1,647 ≈ $1,650 per person

2. Pillar A: Mortality valuation

Pillar A estimates the welfare cost of climate-attributable premature mortality using the Value of a Statistical Life (VSL) framework used in federal regulatory analysis.

The stylized formula is:

A = D × VSL

where:

- D = estimated climate-attributable premature deaths in 2025

- VSL = value of a statistical life

Pillar A is treated as a contemporaneous willingness-to-pay valuation of mortality risk, not as a decomposition of life-years. Because Pillar A values mortality using a contemporaneous VSL, discounting is primarily relevant to Pillar B and to any portion of Pillar C that reflects future streams of lost healthy life rather than same-year welfare loss.

3. Pillar B: Life-expectancy loss

Pillar B captures the welfare loss associated with reductions in healthy life expectancy caused by heat exposure, smoke exposure, chronic disease burdens, and other climate-linked pathways that may not appear as immediate mortality events in a single-year accounting frame.

The stylized formula is:

B = Σ(LYᵢ × VSLY)

where:

- LYᵢ = climate-attributable life-years lost for group i

- VSLY = value of a statistical life-year

Pillar B is constructed as a non-overlapping residual welfare component and is not derived by mechanically decomposing Pillar A’s VSL estimate into life-years. Instead, it captures life-expectancy and health losses not already subsumed within the mortality valuation framework used in Pillar A. Put differently, Pillar A (VSL-based mortality valuation) captures the welfare equivalent of premature mortality as a contemporaneous risk realization, while Pillar B is calibrated to exclude mortality already captured in Pillar A and instead reflects residual life-expectancy and morbidity effects not subsumed by VSL valuation.

4. Pillar C: Morbidity and quality-of-life loss

Pillar C estimates the welfare cost of climate-driven morbidity, including heat-related illness, smoke-related respiratory burdens, mental-health stress, chronic disease aggravation, and other forms of degraded physical and psychological well-being.

The stylized formula is:

C = Σ(Qᵢ × Vᵢ)

where:

- Qᵢ = quantity of climate-attributable morbidity burden for condition i

- Vᵢ = monetized welfare value associated with that burden

This pillar can be operationalized using QALY, DALY, or related health-welfare valuation methods.

D. Summary of Framework 1

The Macroeconomic and Welfare Framework yields the following 2025 estimate:

$1.50T + $0.56T = $2.06T

Per capita:

$2.06T / 340M = $6,059 ≈ $6,050 per person

For a family of four:

4 × $6,050 = $24,200

Framework 1 therefore estimates that climate change imposed a 2025 macro-welfare burden of roughly $2.06 trillion on the United States, equivalent to about $6,050 per person or $24,200 for a family of four.

III. Methodology 2: The Economic and Social Justice Framework

A. Conceptual Architecture

Framework 2 asks a different question. Instead of measuring only the annual economic and welfare burden of climate change, it asks what the ledger would look like if climate damages were valued through a justice and deterrence lens, analogous to legal doctrines that multiply proven damages in response to willful misconduct, fraud, or socially destructive externalization of harm.

This framework begins with the same $1.5 trillion economic damage baseline used in Framework 1, but applies a treble-damages logic to those economic damages only.

Let:

E = Economic Climate Damages = $1.5T

Then the justice framework is:

Justice Cost = E + 3E = 4E

Substituting the 2025 baseline:

$1.5T + 3($1.5T) = $6.0T

Equivalently:

4 × $1.5T = $6.0T

On a per-capita basis:

$6.0T / 340M = $17,647 ≈ $17,600 per person

For a family of four:

4 × $17,600 = $70,400

Why the treble multiplier is applied only to the $1.5T economic burden

The treble-damages multiplier is applied only to the market-facing economic damage ledger ($1.5T), not to the CWAF welfare component ($560B). This choice is intentional. The justice framework is designed as a liability-style multiplier on economic damages—that is, on direct and indirect market harms such as property destruction, insurance destabilization, healthcare spending, public fiscal outlays, productivity loss, and climate-driven price pressures. By contrast, the CWAF already monetizes non-market welfare harms such as mortality risk, life-expectancy degradation, and morbidity-related quality-of-life loss. Trebling those welfare values would risk both conceptual double counting and an analytically awkward punitive replication of already-imputed welfare losses. Accordingly, Framework 2 should be understood as a justice-weighted escalation of the economic climate ledger, not as a trebling of the entire macro-welfare burden.

This framework is therefore not presented as a conventional welfare-economics estimate. It is a normative legal-economic framework designed to reflect accountability, deterrence, and the uneven distribution of climate harm.

B. The Legal Foundation of Treble Damages

Treble damages are a long-established feature of U.S. law in contexts where ordinary compensation is considered inadequate to deter or punish egregious misconduct. They appear most prominently in:

- Antitrust law, including the Sherman Act

- Civil racketeering actions, including RICO-based claims

- False Claims Act enforcement, where fraud against the public fisc can trigger multiplied damages

The logic of treble damages is not merely compensatory. It is also punitive and deterrent. Trebling recognizes that some harms are imposed through conduct sufficiently reckless, deceptive, or socially damaging that ordinary compensation fails to capture either the full social cost or the need for institutional deterrence.

C. Application to Climate Justice

The justice framework applies this legal logic to climate damages on the theory that a substantial share of modern climate costs reflects not only physical climate change, but also delayed mitigation, historic externalization of damages, and sustained campaigns of misinformation or obstruction that prolonged fossil-fuel dependence and delayed adaptation.

Three considerations motivate the treble-damages approach:

1. Willful misconduct and delayed action

If major emitters or institutions knowingly delayed action while externalizing foreseeable climate harms onto the public, then a purely compensatory accounting of damages may understate the true social cost of that conduct.

2. Unequal distribution of harm

Climate damages are not evenly distributed. Lower-income households, communities of color, medically vulnerable populations, outdoor workers, and disaster-prone regions often bear disproportionate burdens. A justice framework therefore recognizes that climate losses are not merely aggregate economic losses but also distributional injuries.

3. Deterrence and accountability

A damages framework that merely reimburses a fraction of direct losses may fail to deter future misconduct. A justice-oriented framework treats climate damages as the basis for a larger accountability regime aimed at shifting incentives, strengthening disclosure, and pricing the cost of willful inaction.

IV. Comparative Analysis

A. Aggregate Results

The two frameworks produce sharply different valuations of the 2025 U.S. climate burden.

| Metric | Framework 1: Macro-Welfare | Framework 2: Justice |

|---|---|---|

| Economic burden baseline | $1.50 trillion | $1.50 trillion |

| Welfare burden (CWAF) | $0.56 trillion | — |

| Treble-damages penalty on economic burden | — | $4.50 trillion |

| Total national cost | $2.06 trillion | $6.00 trillion |

| Cost per capita | $6,050 | $17,600 |

| Cost for family of four | $24,200 | $70,400 |

Framework 1 estimates the full annual burden of climate change on the economy and on human welfare. Framework 2 estimates the justice-weighted accountability cost of climate harm if society chose to treat delayed mitigation and externalized damages as punishable economic injury.

B. Analytical Differences Between the Frameworks

1. Audience and institutional use

Framework 1 is primarily relevant to:

- fiscal policy analysts

- macroeconomists

- central banks

- public-health planners

- federal agencies conducting benefit-cost analysis

Framework 2 is more relevant to:

- litigators

- state attorneys general

- municipal plaintiffs

- tort scholars

- climate-justice advocates

2. Philosophical foundation

Framework 1 measures systemic drag, welfare erosion, and hidden social cost. It asks: What is climate change costing the country in real economic and human terms right now?

Framework 2 measures culpability, deterrence, and social restitution. It asks: What would climate damages look like if society priced not only the injury itself, but also the institutional misconduct that helped produce and intensify it?

3. Risk allocation

Framework 1 reveals the extent to which climate change already functions as a hidden national tax on households, businesses, and governments. Framework 2 goes further by reallocating that burden conceptually back toward those who knowingly profited while imposing climate costs on others.

V. Policy, Legal, and Economic Implications

A. Macroeconomic Policy

The first implication is that GDP alone is no longer an adequate climate accounting tool. A country can rebuild after a flood, spend more on medical care, or borrow more for disaster relief, and those expenditures may still appear as positive economic activity in national accounts even as the underlying social condition worsens.

Incorporating macro-welfare climate accounting into federal analysis would improve:

- Office of Management and Budget benefit-cost analysis

- federal adaptation planning

- public-health prioritization

- insurance and housing policy

- long-run fiscal projections

A climate burden of roughly $2.06 trillion in 2025, or about $6,050 per person, implies that climate change already functions as a material macroeconomic drag on the United States.

B. Climate Litigation and Tort Reform

The second implication is legal. The justice framework provides a conceptual bridge between aggregate climate economics and climate liability. If climate damages are increasingly litigated through state, municipal, and public-nuisance actions, a framework that translates economic harm into a deterrence-oriented damages structure may become increasingly relevant.

This does not mean courts should automatically adopt a 3x multiplier in climate litigation. Rather, it suggests that climate damages can be conceptualized not merely as diffuse acts of nature, but as partly socialized harms linked to historic patterns of concealment, delay, and cost externalization.

C. Socioeconomic Equity

A third implication concerns equity. If the annual climate burden is framed as $17,600 per person under a justice-based model, the economics of adaptation, resilience spending, green infrastructure, household subsidies, and climate restitution look very different. The scale of the burden implies that aggressive decarbonization and resilience investment may be economically justified not merely as environmental policy, but as partial relief from a large and regressive climate tax.

VI. Limitations

Several limitations should be acknowledged.

A. Framework 1 limitations

The macro-welfare framework is a synthetic accounting model rather than a single-source official estimate. Its economic burden baseline aggregates multiple categories of loss that are themselves subject to uncertainty, overlap, and incomplete attribution. The CWAF component similarly relies on bounded welfare estimates rather than a single fully observed national health ledger.

B. Framework 2 limitations

The justice framework is explicitly normative. It is not a standard welfare-economic estimate and should not be confused with a measured national-income loss. Its treble-damages logic is best understood as a legal-economic thought experiment grounded in deterrence and accountability rather than as a conventional national-accounts statistic.

C. Attribution limitations

Not every harmful event in 2025 can be cleanly attributed to climate change, and climate-health pathways remain unevenly measured across disease categories, geographies, and populations. As with all climate-damages accounting, results depend partly on attribution choices, valuation assumptions, and the treatment of overlap among categories.

VII. Conclusion

A. Restatement of Main Findings

This study develops a dual accounting of the 2025 U.S. climate burden.

Under the Macroeconomic and Welfare Framework, climate change imposed an estimated burden of:

$1.50T + $0.56T = $2.06T

equivalent to roughly:

$2.06T / 340M = $6,059 ≈ $6,050 per person

or:

4 × $6,050 = $24,200 for a family of four

Under the Economic and Social Justice Framework, applying a treble-damages logic to the $1.5 trillion economic burden yields:

$1.5T + 3($1.5T) = $6.0T

equivalent to roughly:

$6.0T / 340M = $17,647 ≈ $17,600 per person

or:

4 × $17,600 = $70,400 for a family of four

B. Final Synthesis

Climate change now functions in the United States as both an immediate economic tax and a profound social injustice. The first framework measures what the country is losing in output, health, welfare, and resilience. The second asks what those losses would look like if climate harm were treated not merely as misfortune, but as a large-scale social injury intensified by delayed action, externalized damages, and institutional failure.

The gap between $2.06 trillion and $6.0 trillion is therefore not a contradiction. It reflects two different but complementary questions:

- What is climate change costing the United States right now?

- What should climate damages cost if accountability and deterrence are taken seriously?

C. Future Research Directions

Future work should extend this framework in at least four directions:

- State-level and metropolitan climate-tax estimates, especially for high-risk regions facing acute insurance, flood, heat, or wildfire stress

- Sector-specific justice multipliers, particularly for fossil-fuel litigation and public-finance exposure

- Improved climate-health attribution models, especially for smoke exposure, heat mortality, chronic disease aggravation, and infectious disease pathways

- Dynamic multi-year climate ledgers that track the compounding interaction of direct disaster losses, welfare erosion, and legal liability over time

Appendix A. Summary Tables

A1. Framework 1: Macro-Welfare Burden

| Component | Aggregate Cost | Per Capita |

|---|---|---|

| Economic burden baseline | $1.50 trillion | $4,400 |

| Climate Welfare Accounting Framework (CWAF) | $0.56 trillion | $1,650 |

| Total Framework 1 burden | $2.06 trillion | $6,050 |

A2. CWAF Raw Component Structure

| CWAF Pillar | Low | Central | High |

|---|---|---|---|

| Mortality cost | $225B | $375B | $562.5B |

| Life expectancy loss cost | $40B | $80B | $140B |

| Morbidity / quality-of-life cost | $100B | $180B | $280B |

| Total welfare cost (raw component sum) | $365B | $635B | $982.5B |

Note: The raw central sum of $635B is conservatively adjusted downward in the CWAF headline estimate to approximately $560B to account for overlap risk across mortality, life-year loss, and morbidity channels.

A3. Framework 2: Justice-Based Burden

| Component | Aggregate Cost | Per Capita |

|---|---|---|

| Economic burden baseline | $1.50 trillion | $4,400 |

| Treble-damages penalty on economic burden | $4.50 trillion | $13,200 |

| Total Framework 2 burden | $6.00 trillion | $17,600 |

Appendix B. Formula Summary

Framework 1

- Total Climate Burden (Macro-Welfare) = Economic Burden + Climate Welfare Burden

- $1.50T + $0.56T = $2.06T

- $2.06T / 340M = $6,059 ≈ $6,050 per person

- $4,400 + $1,650 = $6,050

Economic Burden Baseline

- $1.50T / 340M = $4,412 ≈ $4,400 per person

CWAF

- CWAF(raw) = A + B + C

- A = $375B

- B = $80B

- C = $180B

- $375B + $80B + $180B = $635B

- CWAF(adjusted central estimate) ≈ $560B

- $560B / 340M = $1,647 ≈ $1,650 per person

CWAF Pillars

- A = D × VSL

- B = Σ(LYᵢ × VSLY)

- C = Σ(Qᵢ × Vᵢ)

Framework 2

- E = Economic Climate Damages = $1.5T

- Justice Cost = E + 3E = 4E

- $1.5T + 3($1.5T) = $6.0T

- $6.0T / 340M = $17,647 ≈ $17,600 per person

- 4 × $17,600 = $70,400 per family of four

References

Federal valuation guidance: mortality risk, VSL, and benefit-cost analysis

U.S. Department of Transportation. (2021). Departmental Guidance on Valuation of a Statistical Life in Economic Analysis. Office of the Secretary of Transportation. Available at: https://www.transportation.gov/office-policy/transportation-policy/revised-departmental-guidance-on-valuation-of-a-statistical-life-in-economic-analysis

U.S. Department of Transportation. (2021). Valuation of a Statistical Life Guidance. Office of the Secretary of Transportation. Available at: https://www.transportation.gov/resources/value-of-a-statistical-life-guidance

U.S. Department of Transportation. (2025). Economic Values Used in Analyses. Office of the Secretary of Transportation. Available at: https://www.transportation.gov/regulations/economic-values-used-in-analysis

U.S. Environmental Protection Agency. (2010). Guidelines for Preparing Economic Analyses. National Center for Environmental Economics, U.S. EPA, Washington, DC. Available at: EPA Guidelines for Preparing Economic Analyses

U.S. Environmental Protection Agency. (2026). Mortality Risk Valuation. Environmental Economics, U.S. EPA. Available at: https://www.epa.gov/environmental-economics/mortality-risk-valuation

Dockins, C., Maguire, K. B., Newbold, S., Simon, N. B., Krupnick, A., & Taylor, L. O. (2018). What’s in a Name? A Systematic Search for Alternatives to “VSL”. U.S. Environmental Protection Agency, Environmental Economics Working Paper Series, Working Paper No. 2018-01. Available at: https://www.epa.gov/environmental-economics/working-paper-whats-name-systematic-search-alternatives-vsl

Social cost of carbon, climate damages, and climate-economy valuation

Interagency Working Group on the Social Cost of Greenhouse Gases, United States Government. (2021). Technical Support Document: Social Cost of Carbon, Methane, and Nitrous Oxide Interim Estimates under Executive Order 13990. Washington, DC. Available at: Interagency Working Group Technical Support Document

Rennert, K., Errickson, F., Prest, B. C., Rennels, L., Newell, R. G., Pizer, W., Kingdon, C., Wingenroth, J., Cooke, R., Parthum, B., Smith, D., Cromar, K., Diaz, D., Moore, F. C., Müller, U. K., Mendelsohn, R., Anthoff, D., Rose, S., & Waldhoff, S. (2022). “Comprehensive evidence implies a higher social cost of CO₂.” Nature, 610, 687–692.

Carleton, T. A., Jina, A., Delgado, M. T., Greenstone, M., Houser, T., Hsiang, S., Hultgren, A., Jisu, K., McCusker, K., Nath, I., Rising, J., Rode, A., Seo, H. K., Viaene, A., Yuan, J., & Zhang, A. T. (2022). “Valuing the global mortality consequences of climate change accounting for adaptation costs and benefits.” The Quarterly Journal of Economics, 137(4), 2037–2105.

U.S. climate impacts, health burden, and national assessment context

U.S. Global Change Research Program. (2023). Fifth National Climate Assessment. Washington, DC: U.S. Global Change Research Program. Available at: https://nca2023.globalchange.gov/

Romanello, M., Di Napoli, C., Green, C., Kennard, H., Lampard, P., Scamman, D., Walawender, M., Ali, Z., et al. (2024). “The 2024 report of the Lancet Countdown on health and climate change: facing record-breaking threats from delayed action.” The Lancet.

(Use the final journal citation details/DOI exactly as published in the version you relied on.)

World Health Organization. (2023). Climate change and health. Geneva: World Health Organization. Available at: https://www.who.int/news-room/fact-sheets/detail/climate-change-and-health

Legal and justice-framework authorities for treble damages and climate accountability framing

Clayton Act, 15 U.S.C. § 15. Private antitrust actions; treble damages provision. Available at: https://www.law.cornell.edu/uscode/text/15/15

Racketeer Influenced and Corrupt Organizations Act (RICO), 18 U.S.C. § 1964(c). Civil remedies; treble damages provision. Available at: https://www.law.cornell.edu/uscode/text/18/1964

False Claims Act, 31 U.S.C. §§ 3729–3733. Civil liability and damages provisions for fraud against the United States. Available at: https://www.law.cornell.edu/uscode/text/31/3729