“The greater risk is a gradual degradation of living standards if adaptation is delayed.“

by Daniel Brouse

Introduction

Climate change is often discussed as if it will either produce an imminent societal collapse or, conversely, have little economic consequence. Neither view is supported by the physical science.

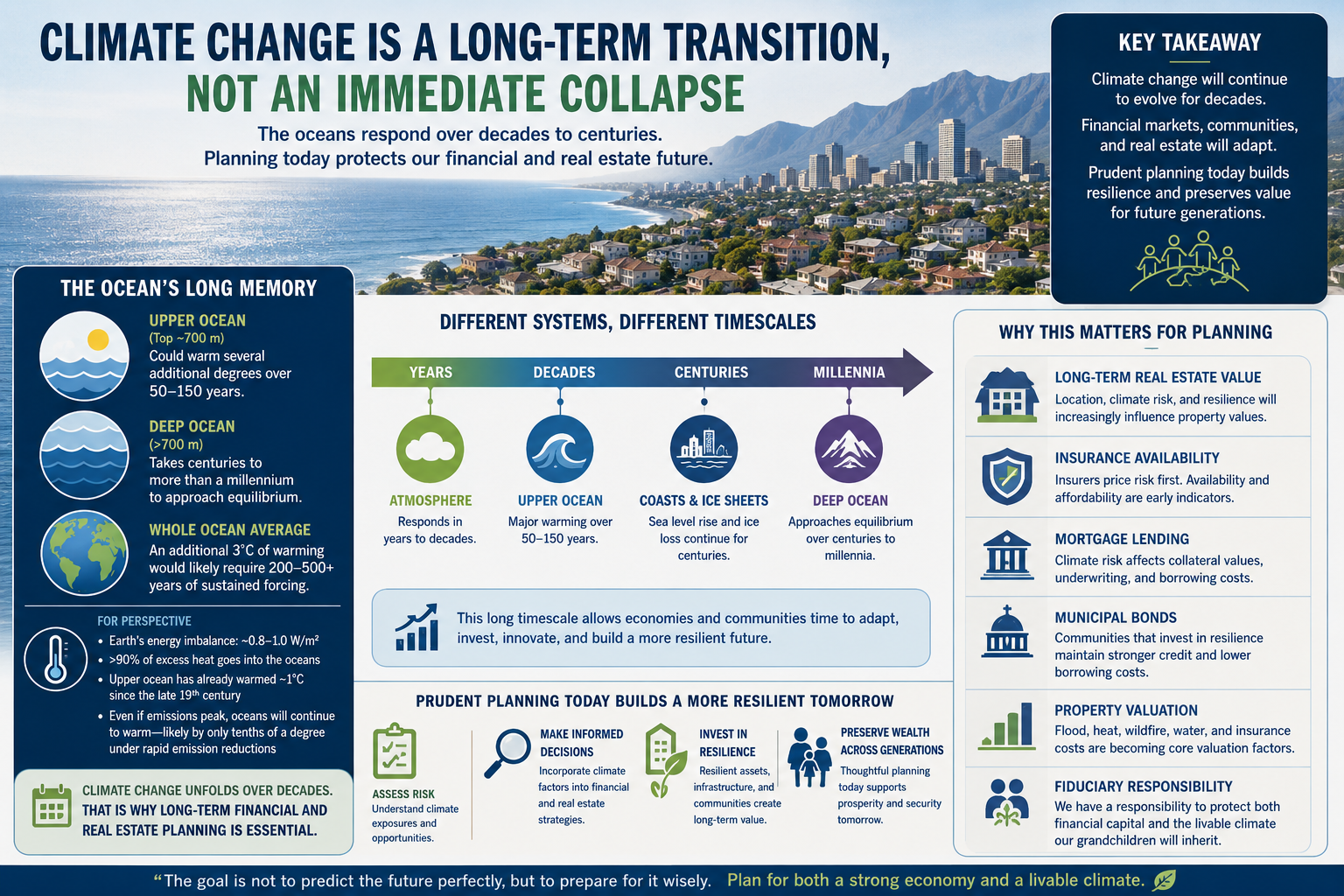

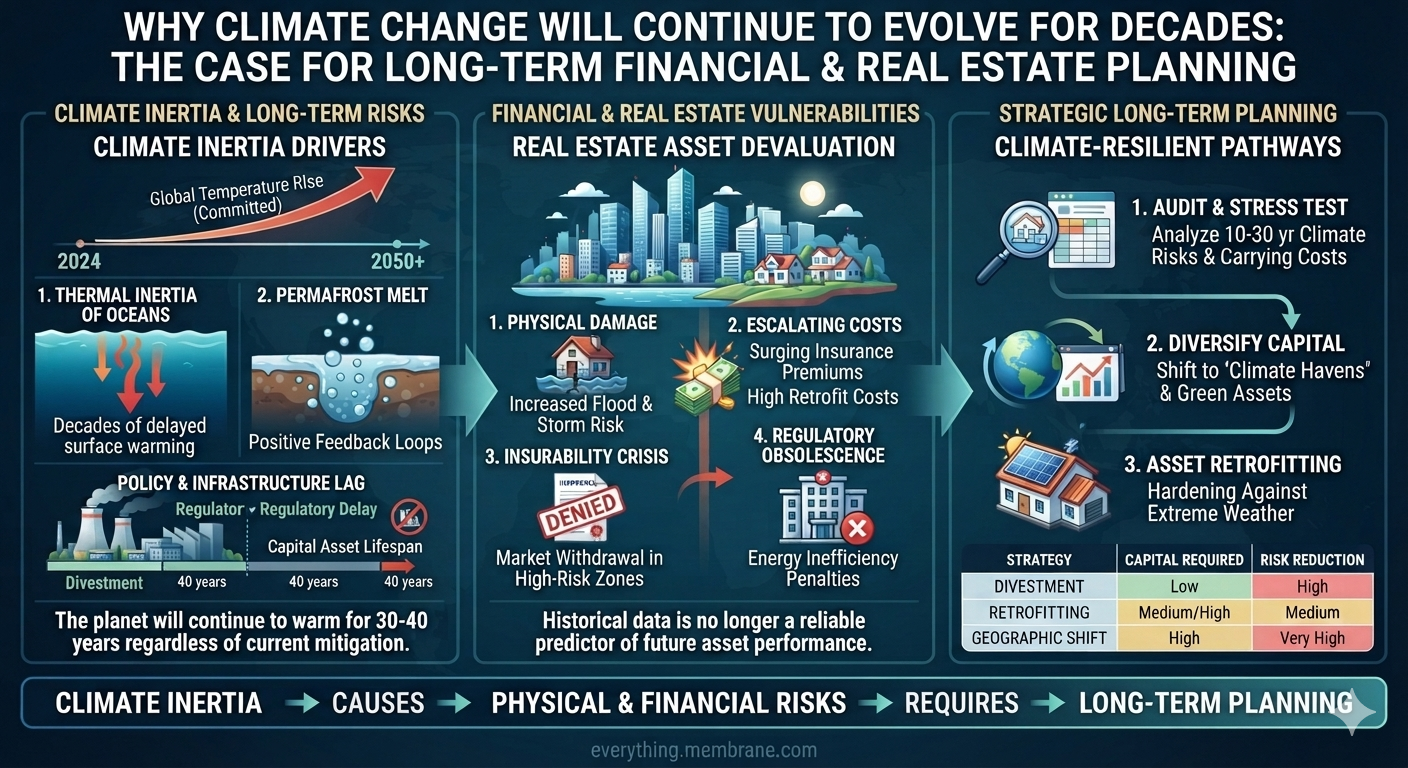

The Earth’s climate system responds over multiple timescales. While the atmosphere reacts relatively quickly to changes in greenhouse gas concentrations, the oceans—the planet’s largest heat reservoir—respond much more slowly. This difference, known as thermal inertia, means that many of the economic consequences of climate change will continue to unfold over decades, regardless of whether emissions peak today or several years from now.

For investors, homeowners, businesses, insurers, lenders, and governments, this distinction is critical. The evidence points not toward an immediate collapse of the global economy, but toward a long period of increasing environmental risks that will progressively reshape financial markets and real estate values.

The Ocean’s Long Memory

If greenhouse gas concentrations remained near current levels long enough to maintain today’s radiative forcing, it would likely take many decades to centuries for the global ocean to warm by an additional 3°C.

Current scientific understanding suggests:

- The upper ocean (roughly the top 700 meters) could warm several additional degrees over approximately 50–150 years.

- The deep ocean requires centuries to more than a millennium to approach equilibrium.

- The global ocean average would likely require several centuries of sustained forcing to warm another 3°C.

More than 90% of Earth’s excess heat enters the oceans, giving the climate system enormous momentum.

Even if atmospheric temperatures stabilize, sea level rise, marine heat waves, glacier retreat, and many coastal impacts continue because the oceans continue redistributing heat.

Climate change therefore behaves less like flipping a switch and more like steering an aircraft carrier. Once underway, changes continue for decades.

Why This Does Not Mean Immediate Economic Collapse

The nonlinear acceleration of climate change does not imply that modern economies disappear within a few years.

Economic systems continually adapt.

History demonstrates remarkable resilience through world wars, financial crises, pandemics, technological revolutions, and natural disasters. Markets evolve. Capital reallocates. Infrastructure is rebuilt. New technologies emerge.

Climate change represents another major structural transformation—not an instantaneous end to economic activity.

The greater risk is a gradual degradation of living standards if adaptation is delayed.

Financial Markets Price Risk—They Do Not Ignore It

Financial markets constantly evaluate future expectations.

Investors already incorporate:

- Inflation

- Interest rates

- Technological disruption

- Demographics

- Political risk

- Corporate earnings

Climate risk is becoming another measurable input.

Rather than causing markets to cease functioning, climate change increasingly changes how capital is allocated.

Investment flows are likely to favor:

- Resilient infrastructure

- Water management

- Energy efficiency

- Distributed power systems

- Climate-resilient agriculture

- Advanced building technologies

- Adaptation engineering

Markets rarely stop functioning.

They reprice risk.

Mortgage Lending in a Changing Climate

Mortgage lending has always depended upon one fundamental assumption:

The collateral will retain value over the life of the loan.

Most residential mortgages extend 15 to 30 years.

Commercial financing often spans decades.

Those time horizons now overlap directly with accelerating climate risks.

Lenders are increasingly evaluating:

- Flood exposure

- Wildfire probability

- Coastal erosion

- Extreme heat

- Water availability

- Infrastructure resilience

- Local adaptation policies

Climate risk is becoming credit risk.

Properties with increasing exposure may experience:

- Higher insurance costs

- Larger reserve requirements

- Lower loan-to-value ratios

- Increased underwriting scrutiny

- Higher borrowing costs

Conversely, resilient communities with strong infrastructure may receive more favorable financing because they present lower long-term risk.

Climate-informed lending is simply modern risk management.

Insurance Availability May Become the First Market Signal

Insurance companies often detect climate risk before property markets do.

Unlike homeowners, insurers continuously update catastrophe models using the latest observations and loss data.

When risks increase, insurers respond by:

- Raising premiums

- Increasing deductibles

- Restricting coverage

- Reducing policy limits

- Withdrawing from selected markets

Recent developments in wildfire-prone states, hurricane-exposed coastlines, and hail-prone regions illustrate this trend.

In many communities, insurance affordability—not property damage itself—may become the first significant economic consequence of climate change.

Without affordable insurance:

- Mortgage financing becomes more difficult.

- Homeownership becomes more expensive.

- Property values may weaken.

- Municipal tax bases can come under pressure.

Insurance increasingly serves as an early warning system for long-term climate risk.

Municipal Bonds and Local Government Finance

Climate resilience is increasingly becoming a municipal finance issue.

Cities and counties finance much of their infrastructure through municipal bonds.

Those bonds ultimately depend upon:

- Stable tax revenues

- Economic growth

- Reliable infrastructure

- Sustainable operating costs

As climate risks increase, municipalities may require additional investments in:

- Flood control

- Stormwater systems

- Water supply

- Cooling infrastructure

- Grid modernization

- Emergency services

- Road and bridge resilience

Communities that invest proactively may maintain stronger credit quality over time.

Communities that defer adaptation could face rising maintenance costs, increasing insurance expenses, and pressure on their fiscal health.

For municipal investors, climate resilience increasingly becomes part of long-term credit analysis.

Property Valuation Is Becoming Dynamic

Historically, property valuation focused on:

- Location

- Schools

- Transportation

- Employment

- Neighborhood quality

Climate is becoming another location characteristic.

Future valuation models will likely incorporate increasing amounts of climate-related information, including:

- FEMA flood maps

- Local flood history

- Heat exposure

- Wind risk

- Wildfire potential

- Water reliability

- Insurance costs

- Building resilience

- Community adaptation investments

Properties will not simply gain or lose value because of climate change.

Rather, markets will increasingly differentiate between properties based on their long-term resilience.

The result is likely to be greater divergence between communities that prepare and those that do not.

Investment Implications

Because climate impacts unfold over decades, financial planning becomes more—not less—important.

Assuming there will be “no economy” several years from now is neither supported by economic history nor by climate science.

Instead, investors should recognize that long-term wealth preservation increasingly depends upon understanding long-term environmental risk.

That includes:

- Diversified investment portfolios.

- Climate-informed real estate decisions.

- Appropriate insurance coverage.

- Infrastructure resilience.

- Geographic diversification.

- Long-term retirement planning.

Planning remains one of the strongest tools available for reducing future financial risk.

Fiduciary Responsibility Across Generations

Every generation inherits assets built by those before it.

Likewise, every generation passes assets forward.

That fiduciary responsibility extends beyond investment portfolios.

It includes:

- Homes.

- Communities.

- Infrastructure.

- Businesses.

- Natural resources.

- Financial systems.

Protecting both environmental and financial capital is not a contradiction.

It is prudent stewardship.

Planning for climate risk is no different than planning for inflation, demographic change, technological disruption, or changing interest rates.

Responsible investors prepare for foreseeable risks rather than assuming those risks either do not exist or will immediately end the economic system.

Conclusion

Climate science indicates that many impacts will continue evolving over decades because Earth’s oceans absorb and release heat slowly.

That long timescale does not support predictions of imminent economic collapse.

Instead, it points toward an extended period during which markets continuously adapt by repricing risk, directing capital toward resilience, and rewarding long-term planning.

For homeowners, investors, lenders, insurers, businesses, and governments, the challenge is not deciding whether there will be an economy.

The challenge is helping shape an economy that is both financially resilient and environmentally sustainable.

The goal is not simply to leave future generations a larger investment portfolio.

It is to leave them both a livable climate and an economy capable of supporting opportunity for decades to come.