by Daniel Brouse

October 14, 2025

On October 14, 2025, in a speech delivered in Philadelphia, Federal Reserve Chair Jerome Powell hinted at a significant policy shift — one that could reshape the financial landscape for years to come. Powell indicated that the Fed may soon end its balance sheet reduction program, effectively pausing Quantitative Tightening (QT) and signaling the potential return of Quantitative Easing (QE).

The motivation, he said, lies in growing concern over labor market weakness and the need to provide “stability” amid economic uncertainty. Powell described the move as “QE-like” and acknowledged the risks of persistent inflation, while emphasizing the importance of tracking a broad set of data — particularly state-level employment figures — in the absence of timely federal economic reports.

In practical terms, Powell also suggested that the Fed would begin buying U.S. Treasuries again. For investors, businesses, and consumers, this represents a major turning point — and a deeply troubling one.

What Is Quantitative Easing (QE)?

In simple terms, QE is money creation. The Federal Reserve purchases financial assets — usually Treasury bonds or mortgage-backed securities — to inject liquidity into the banking system and push long-term interest rates lower. While this can provide short-term relief to credit markets, it almost always comes with serious long-term consequences: asset bubbles, wealth inequality, and inflationary pressure.

Fiscally conservative economists, including many Republicans, have traditionally opposed QE for precisely this reason — it’s artificial stimulus that distorts markets and devalues currency. Ironically, the largest expansions of QE have occurred under Republican administrations, particularly under Presidents Bush and Trump.

At its core, QE works like this:

* The U.S. Treasury issues debt in the form of bonds.

* The Federal Reserve buys those bonds using newly created money.

The result is a loop of monetized debt, where the government effectively funds itself by printing dollars through the Fed’s balance sheet. When considering the full fiscal picture, the real U.S. debt burden should include both the national debt and the Federal Reserve’s assets — a combined total of roughly $44.5 trillion:

$37,887,475,445,601 (national debt)

+ $6,608,000,000,000 (Federal Reserve assets)

= $44.495 trillion owed by U.S. taxpayers

That’s the true figure Americans are on the hook for. And the question remains: how will it ever be repaid?

The History of QE

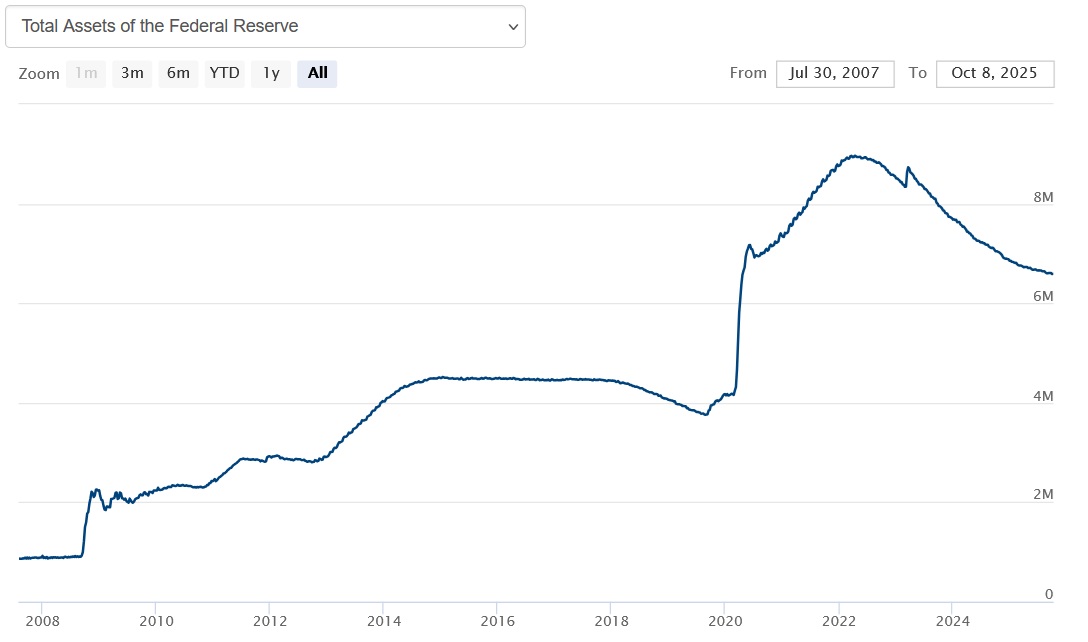

The Federal Reserve first launched Quantitative Easing in November 2008, during the Great Recession, under President George W. Bush. Known as QE1, the program focused on purchasing mortgage-backed securities and agency debt to stabilize collapsing credit markets when interest rates were already near zero.

This initial cycle expanded the Fed’s balance sheet to approximately $4.5 trillion. By late 2019, the Fed began to unwind those holdings — allowing assets to “roll off” as they matured — marking the start of Quantitative Tightening (QT). However, the onset of the COVID-19 pandemic in 2020, under President Trump, triggered an unprecedented new wave of Quantitative Easing (QE), which rapidly expanded the balance sheet to nearly $9 trillion, the highest level in U.S. history. Many economists attribute a significant portion of the 2021–2022 inflation surge to this Trump-era QE, which flooded the financial system with liquidity and fueled speculative bubbles across housing, equities, and commodities.

In 2022, under President Biden, the Fed began a gradual process of balance sheet reduction, marking the start of Quantitative Tightening (QT) reducing the Fed’s assets to $6.6 trillion.

Now, just a few years later, Powell’s comments suggest a reversal of that policy — a return to money printing at a time when inflation remains above target and fiscal deficits are exploding.

QE Today: The Warning Signs

Powell’s latest remarks should set off alarm bells across the financial community. Reintroducing QE in the current environment — with massive fiscal deficits, high consumer debt, and lingering inflation — is not a stabilizing policy. It’s a recipe for economic disaster.

By artificially lowering rates and inflating asset prices, the Fed risks fueling another speculative bubble — one that could end in catastrophic wealth destruction, job loss, and financial contagion. Meanwhile, the federal government’s relentless spending ensures that each round of QE only digs the hole deeper.

This is not monetary stability. It’s the illusion of prosperity — a temporary sugar high before a historic crash.

If the Fed follows through with this plan, the outcome is predictable: rising inequality, eroding purchasing power, and ultimately what could become the Greatest Depression in U.S. history.

Creative Destruction in the Age of AI: How Endogenous Growth Theory Explains AI Stock Market Bubble